Introduction

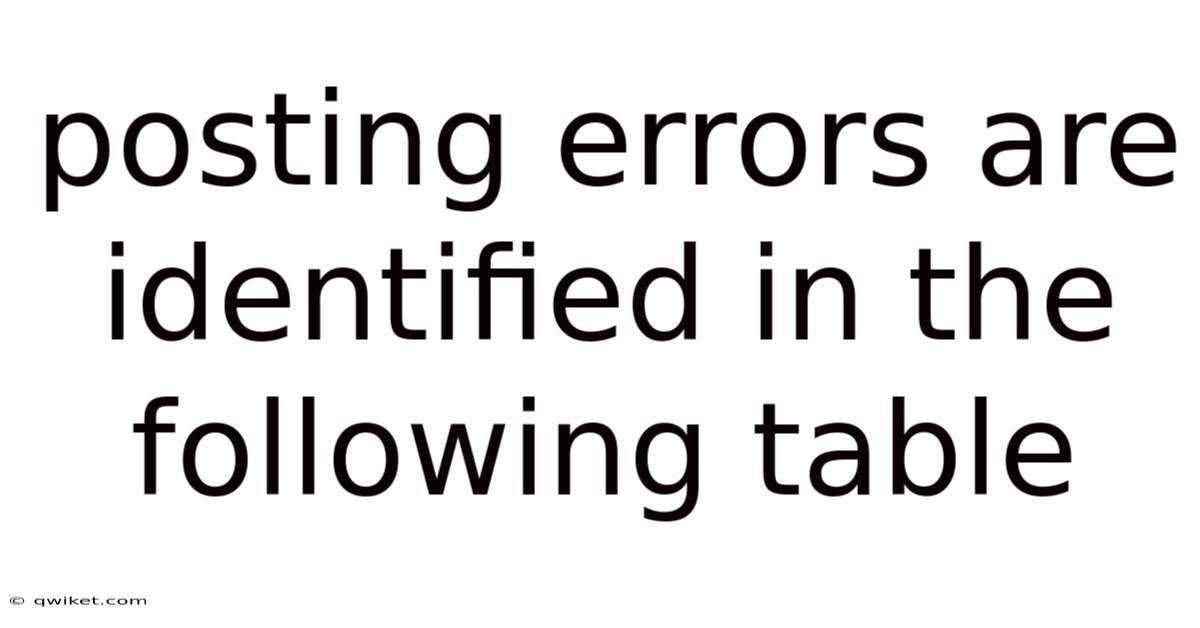

In accounting, posting errors are mistakes made when transferring information from source documents or journals to the general ledger. The table below illustrates typical posting errors that organizations encounter, and the subsequent sections explain how to identify, analyze, and correct each type. Even a single incorrect entry can distort financial statements, affect decision‑making, and trigger compliance issues. By mastering these concepts, accountants and bookkeepers can safeguard the integrity of their financial data and maintain confidence among stakeholders.

| Error Code | Description | Typical Cause | Impact on Financials |

|---|---|---|---|

| E‑01 | Transposition of digits (e.Even so, g. , 540 recorded as 450) | Manual entry slip, hurried data input | Overstated or understated revenue/expense, affecting net income |

| E‑02 | Wrong account posted (e.g., debit to Supplies instead of Inventory) | Misunderstanding of chart of accounts, similar account numbers | Misclassification leads to inaccurate asset or expense balances |

| E‑03 | Omitted posting (transaction never entered) | Overlooked journal line, system glitch | Incomplete financial picture, potential tax under‑reporting |

| E‑04 | Duplicate posting (same transaction posted twice) | Copy‑and‑paste error, batch processing repeat | Inflated balances, overstated expenses or revenues |

| E‑05 | Incorrect posting date (e.g. |

The following sections dig into each error type, illustrate detection techniques, and propose systematic correction procedures Not complicated — just consistent..

1. Transposition Errors (E‑01)

How they occur

Transposition errors happen when two adjacent digits are swapped during manual entry. Here's one way to look at it: a sales invoice of $5,400 might be recorded as $540 or $5,040. In high‑volume environments, these slips are surprisingly common.

Detection methods

- Variance analysis: Compare month‑over‑month trends; a sudden dip or spike may hint at a transposition.

- Digit‑sum test: For amounts ending in 0 or 5, adding the digits should produce a predictable remainder when divided by 9.

- Automated validation rules: Set up system alerts for entries where the absolute difference between the posted amount and the source amount exceeds a predefined threshold (e.g., 5%).

Correction steps

- Locate the original source document (invoice, receipt).

- Verify the correct amount and note the erroneous posting reference.

- Create a reversal journal for the incorrect entry (debit → credit, credit → debit).

- Post a new, accurate journal entry with the correct amount.

- Document the correction in the audit trail, citing the error code E‑01.

2. Wrong Account Posted (E‑02)

Why it happens

Account numbers that are numerically close (e.g., 1200 – Inventory vs. 1210 – Supplies) can be confused, especially when using drop‑down menus without clear descriptions.

Detection methods

- Trial balance review: Sudden, unexplained increases in a particular expense or asset line may indicate misposting.

- Account mapping reports: Cross‑reference posted transactions against the chart of accounts hierarchy; mismatches surface quickly.

- Exception reports: Generate reports that flag entries where the account type (asset, liability, equity) does not align with the transaction nature.

Correction steps

- Identify the correct account based on the source document’s purpose.

- Reverse the incorrect entry (using a journal entry that mirrors the original).

- Re‑post the transaction to the appropriate account.

- Update any supporting documentation to reflect the change and annotate with E‑02.

3. Omitted Posting (E‑03)

Common scenarios

A purchase order may be approved, but the corresponding invoice never reaches the ledger due to a missed workflow step or a system integration failure.

Detection methods

- Three‑way match: Compare purchase orders, receiving reports, and invoices; any missing link signals an omission.

- Aging reports: Unrecorded liabilities will not appear in the accounts payable aging, prompting a review.

- Reconciliation gaps: When bank statements reconcile but the ledger shows a shortfall, investigate for omitted entries.

Correction steps

- Retrieve the missing source document.

- Create a new journal entry reflecting the transaction in the correct period.

- Adjust any related accruals if the omission impacted period‑end estimates.

- Record the action under E‑03 for future audit reference.

4. Duplicate Posting (E‑04)

How duplication creeps in

Batch imports, especially when a file is re‑uploaded after a failure, can cause the same transaction to be posted twice And that's really what it comes down to..

Detection methods

- Duplicate detection queries: Search for identical amounts, dates, and reference numbers within a short time window.

- Reconciliation differences: A duplicated expense will cause the trial balance to be out of balance by the amount of the duplicate.

- Audit logs: Review system logs for multiple posting attempts of the same transaction ID.

Correction steps

- Verify that the entries are true duplicates (same source, amount, and description).

- Void or delete the redundant entry, following the organization’s policy for voiding (often a reversal journal).

- Ensure the remaining entry is correctly linked to the original source document.

- Mark the incident as E‑04 and note preventive measures (e.g., lock file after successful import).

5. Incorrect Posting Date (E‑05)

Why timing matters

Accrual accounting requires that revenues and expenses be recognized in the period they are earned or incurred. Posting a December sale in January misstates both periods’ results.

Detection methods

- Cut‑off testing: Review transactions around period end to ensure they belong to the correct month.

- Period‑balance comparison: Sudden spikes on the first day of a new period may indicate mis‑dated entries.

- System controls: Enable date‑range validation that warns when a posting date falls outside the open period.

Correction steps

- Determine the correct period based on the transaction date on the source document.

- Reverse the entry with the incorrect date.

- Re‑post the transaction using the accurate posting date.

- If the incorrect date falls in a closed period, obtain necessary approvals and follow the organization’s adjusting entry protocol, documenting as E‑05.

6. Currency Conversion Error (E‑06)

Typical pitfalls

When converting foreign‑currency invoices, using an outdated exchange rate or entering the rate in the wrong direction (multiply instead of divide) skews the local‑currency amount.

Detection methods

- Rate comparison: Cross‑check the rate used against the official rate on the invoice date.

- Variance analysis: Large foreign‑currency gains or losses without supporting documentation raise red flags.

- Automated conversion tools: Ensure the accounting software pulls the correct rate automatically.

Correction steps

- Retrieve the original foreign‑currency invoice and the correct exchange rate for the invoice date.

- Calculate the accurate local‑currency amount.

- Reverse the erroneous entry and post a corrected one using the proper rate.

- Record the correction under E‑06, and if the error generated a foreign‑exchange gain/loss, adjust the related accounts accordingly.

7. Reversal Posted to Wrong Side (E‑07)

What it looks like

A reversal meant to offset a previous entry is entered on the same side (e.g., credit instead of debit), leaving the original amount untouched.

Detection methods

- Trial balance review: The balance of the affected account remains unchanged despite a reversal entry.

- Reversal reports: Compare original and reversal entries; mismatched debit/credit pairs reveal the issue.

- System alerts: Some ERP modules flag reversals that do not neutralize the original amount.

Correction steps

- Identify the original transaction and the incorrect reversal.

- Void the faulty reversal.

- Create a new reversal with the correct debit/credit orientation.

- Document the fix as E‑07 and verify that the net effect on the account is zero.

8. Partial Amount Posted (E‑08)

Situations that cause it

When a payment is split across multiple checks, only one portion may be recorded, leaving the remainder unposted And it works..

Detection methods

- Bank reconciliation: Compare cleared checks with posted amounts; any discrepancy flags a partial posting.

- Aging of receivables/payables: Outstanding balances that should be settled indicate missing portions.

- Payment application reports: Look for invoices with “partial” status that have not been fully applied.

Correction steps

- Locate the full payment documentation (all checks, electronic transfers).

- Post the missing portion as a separate entry or adjust the original entry to reflect the total amount.

- Reconcile the account to ensure the total matches the source documents.

- Log the correction under E‑08.

9. Incorrect Reference Number (E‑09)

Why reference integrity matters

Accurate linking between invoices, purchase orders, and ledger entries creates a reliable audit trail. A wrong reference number can break this chain.

Detection methods

- Reference‑validation reports: Run queries that compare ledger reference numbers against existing PO/invoice numbers.

- Document matching: Manually verify a sample of entries to ensure the reference aligns with the source.

- Audit trail inspection: Discrepancies in reference fields often surface during internal audits.

Correction steps

- Identify the correct reference number from the original document.

- Edit the ledger entry (if the system permits) or reverse and repost with the proper reference.

- Annotate the change with E‑09 and update any supporting spreadsheets or dashboards.

10. Posting to a Closed Period (E‑10)

Risks involved

Most accounting systems lock periods after financial statements are issued. Posting to a closed period can compromise the integrity of already‑published reports.

Detection methods

- System error messages: Attempted postings will generate alerts indicating the period is locked.

- Post‑close review: Compare the ledger after closing to the approved statements; any new entries signal a breach.

- Access logs: Review who attempted to post and why.

Correction steps

- Obtain approval from management or the audit committee to adjust the closed period.

- Create an adjusting entry in the current open period that references the original period (e.g., “Adjustment – Prior Period”).

- Clearly note the reason and error code E‑10 in the entry description.

- Update the period‑close checklist to prevent future unauthorized postings.

FAQ

Q1: How can I prevent posting errors from recurring?

Implement a combination of segregation of duties, automated validation rules, and periodic training. Regularly review exception reports and enforce a double‑check policy for high‑value transactions Worth keeping that in mind..

Q2: Should I correct errors in the same period they occurred?

Ideally, yes. Corrections made in the original period preserve the accuracy of historical financial statements. If the period is closed, use adjusting entries in the current period and disclose the correction in the notes.

Q3: What documentation is required for each correction?

Maintain the original source document, a clear description of the error (including the error code), the reversal journal, the corrected journal, and any management approvals. This creates a transparent audit trail.

Q4: Can accounting software automatically detect all these errors?

Modern ERP systems can flag many issues (duplicate detection, date validation, currency rate mismatches). Still, human oversight remains essential for nuanced errors such as wrong account selection or reference mismatches.

Q5: How do posting errors affect tax reporting?

Misstated revenues or expenses can lead to under‑ or over‑payment of taxes. Prompt identification and correction, along with proper disclosure, mitigate the risk of penalties.

Conclusion

Posting errors, though often perceived as minor clerical slips, have the potential to ripple through an organization’s financial statements, compliance posture, and strategic decision‑making. By systematically categorizing errors—E‑01 through E‑10—and applying targeted detection and correction procedures, accounting teams can dramatically reduce the incidence of inaccurate postings That's the whole idea..

Key takeaways include:

- Vigilant monitoring through variance analysis, exception reports, and reconciliations.

- solid internal controls such as segregation of duties, approval hierarchies, and locked periods.

- Clear documentation of each correction, using standardized error codes for traceability.

When these practices become embedded in the daily workflow, the likelihood of posting errors diminishes, and the reliability of financial information strengthens. This not only satisfies auditors and regulators but also empowers management with trustworthy data for growth‑oriented decisions.